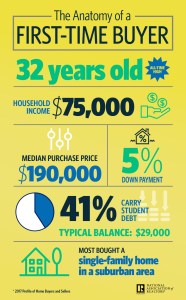

Experts’ home sale inventory forecasts for the spring echo expectations from recent years. And in some regions, it could be a very competitive home buyer market. Affordability is likely to be a major issue according to CoreLogic’s chief economist Frank Nothaft (Peering into the Housing and Mortgage Outlook with 20/20 Vision; corelogic.com; December 5,2019). The CoreLogic Home Price Index predicts that 2020 home prices will increase more than they did during 2019. Lower priced homes will likely appreciate at a much higher rate than upper bracket and luxury homes. Buyers should have their home buying strategies in mind when looking for homes.

Many first-time home buyers may become discouraged and decide to continue renting. However, renting is expected to be less affordable in 2020. CoreLogic’s Single-Family Rent Index indicates that rents are increasing at double the rate of inflation. So, although renting may seem like the default fallback, it may be the more expensive option. A combination of increasing rent, a continuing good economy, and historically low mortgage rates are expected to be the catalyst for home buyers to get into the market.

If you’re a home buyer, the 2020 housing market outlook may sound daunting. Although you may be anticipating something akin to the Game of Thrones this spring, take heart because planning and having home buying strategies can help your home buying success.

Talk to a mortgage lender. One of the worst feelings is finding out a seller took another offer because your offer didn’t have a financing letter. Not identifying a lender and securing an approval letter before looking at homes is a strategic error, especially if you need to move fast on making an offer. Having awesome credit scores, a good income, and savings in the bank, means nothing to a home seller unless a mortgage professional confirms this with a mortgage approval letter.

Work out a home buying budget. Consult financial professionals, such as your financial planner or CPA to review income, assets, and debts to determine a realistic housing budget. In deciding on your housing budget, consider monthly mortgage payments, HOA or condo fees, property tax, insurance, utilities, maintenance, etc. Your loan officer can help determine a home price range based on your monthly housing budget. Although, your home buying budget may be less than the maximum mortgage amount for which you qualify, don’t be tempted to go beyond your budget. Sticking to your budget can help you avoid “buyer’s remorse.”

Although the national housing market is portrayed as very competitive for home buyers, CoreLogic’s Nothaft suggests that local neighborhood markets can differ widely. As a home buyer, keep an open mind and consider a wider home search area. Consider all your home buying options, including new construction, and the possibility of doing an FHA 203k renovation.

One of the most important home buying strategies is to choose your Realtor carefully, as not all agents are the same. Hookup with an experienced full-time real estate agent. Empirical research studies indicate that a seasoned, veteran agent can make a positive impact on your home purchase. Experienced agents understand the nuances of negotiating and can make your home buying experience more efficient. Full-time agents know the market, which is an asset during your home search. Don’t just rely on the first agent you meet at an open house, or finding an agent on the internet. Talk to several (or more) Realtors to determine if they’re a good fit for your goals. Make sure the agent you hire has your best interests in mind when searching homes and negotiating.

Original article is published at https://dankrell.com/blog/2020/01/10/home-buying-strategies-2020/

By Dan Krell

Copyright© 2019

If you like this post, do not copy; instead please:

link to the article,

like it on facebook

or re-tweet.

Disclaimer. This article is not intended to provide nor should it be relied upon for legal and financial advice. Readers should not rely solely on the information contained herein, as it does not purport to be comprehensive or render specific advice. Readers should consult with an attorney regarding local real estate laws and customs as they vary by state and jurisdiction. Using this article without permission is a violation of copyright laws.